The mobility benefit for everyone

Our mobility budget is individually configurable, allowing you to subsidise all types of transportation for work or personal use on a monthly basis. In some cases, this can be done tax-free.

Support all types of mobility. With just one click.

A benefit for everyone

Offer your team the flexibility they need. Regardless how you get to work, all types of transport are accepted.

Reward sustainability

Unlike fuel cards or company cars, Circula can also be used to subsidise environmentally friendly transport.

Easy to roll out

Unlike fuel cards or company cars, Circula can also be used to subsidise environmentally friendly transport.

Everywhere on the road.

All costs considered.

All costs considered.

Tax-free or tax-optimised

Public transport has been completely tax-free since 2019. We offer two tax models so that you have the option of subsidising all types of transport.

5 simple stepsto a mobility budget

Invite users and assign benefits

Admins laden neue Nutzer ein und weisen ihnen bestimmte Benefits über die Funktion „Benefits Gruppen“ zu.

Submit receipts via app

Mitarbeitende reichen die Belege für ihre monatlichen Mobilitätsausgaben einfach per App ein.

.avif)

Verification and net wage optimisation

We check all submitted receipts for legal compliance and calculate the maximum net wage optimisation.

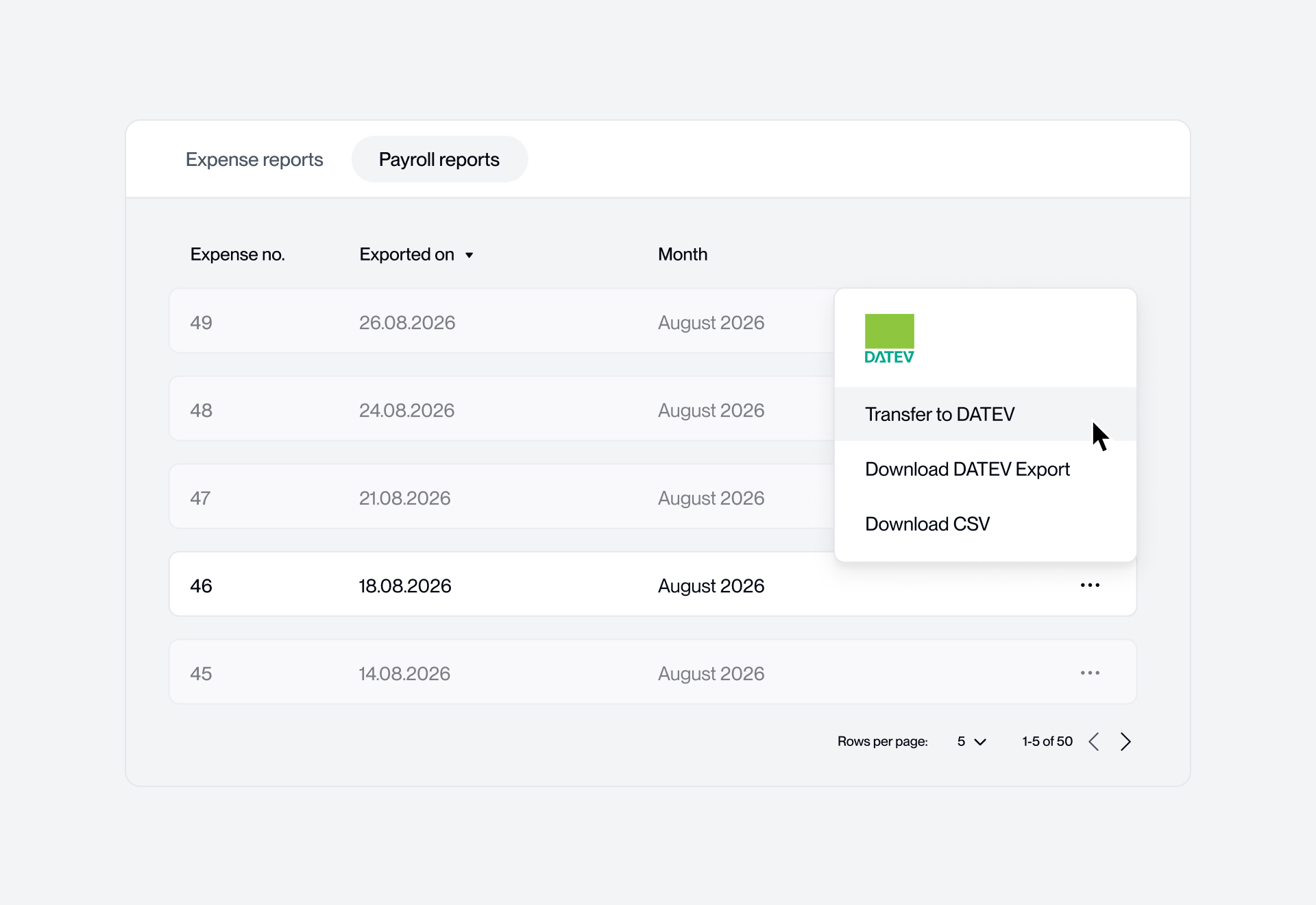

Data transfer to payroll accounting

Die Schnittstelle zu DATEV Lohn & Gehalt oder DATEV LODAS ist inklusive. Übertragen Sie die Daten mit nur einem Klick.

Payment with the next salary

Die eingereichten Kosten werden mit dem nächsten Gehalt erstattet. Alle ausgezahlten Benefits werden auf den Gehaltsnachweisen rechtskonform aufgeführt.

You don't have to be a tax expert to roll out a benefits programme that reaches the people in your company. You just need to know what's important to them. We'll do the rest.

7,000 positive reviews show our customers' love for Circula.

Compliance doesn’t have to be complicated.

Not even in HR. We will show you how easy it is to roll out your individual benefits program.

Do you have any questions?

Yes, employees can submit fuel expenses in the "private transport" category – even for private trips in a car. Note that these costs must be taxed normally.

All journeys by public transport within Germany are tax-free. The usual taxes are paid on journeys by individual transport (e.g. cab, scooter, car sharing) and long-distance transport (ICE, IC).

Exceptions: If the trip is a commute to work made by long-distance transportation, taxes are not due for that trip.

Companies are free to set the amount they want to make available to their employees. This way you remain flexible and offer your employees an individual and unique benefit.

We basically offer two tax models for our Mobility Benefit. As a company, you choose one of the two models: a) completely tax-free or b) both tax-free and taxed at a flat rate of 25%. In the first model, only all public transport journeys and long-distance business journeys (commuting journeys) are subsidised. In the second model, individual transport (e.g. car sharing, e-scooters, e-bikes) and private long-distance journeys are also subsidised.

Furthermore, according to § 40 para. 2 sentence 2 no. 2 EStG, there is the possibility of taxing remuneration that would be tax-exempt according to § 3 no. 15 EStG at a flat rate of 25% (option), with the consequence of reducing the distance allowance

No, employees are free to decide which trips they use their budget for - whether private or work-related is irrelevant. Nevertheless, it must be clearly distinguished from a business trip, business trips cannot be charged or accounted for with the mobility budget. Business trips can be settled with Circula Expenses.

In principle, all means of transport are allowed. However, there are two models based on tax differences that can be applied to different employees or groups of employees in the company: a) completely tax-free and b) partly tax-free, partly taxed. Public transport and long-distance public commuting (not in a car) are tax-free on the part of the legislator, but private long-distance and individual transport, e.g. car sharing, e-scooters, are taxed normally.

We basically offer two tax models for our Mobility Benefit. As a company, you choose one of the two models: a) completely tax-free or b) both tax-free and taxed at a flat rate of 25%. In the first model, only all public transport journeys and long-distance business journeys (commuting journeys) are subsidised. In the second model, individual transport (e.g. car sharing, e-scooters, e-bikes) and private long-distance journeys are also subsidised.

Furthermore, according to § 40 para. 2 sentence 2 no. 2 EStG, there is the possibility of taxing remuneration that would be tax-exempt according to § 3 no. 15 EStG at a flat rate of 25% (option), with the consequence of reducing the distance allowance